CMPDI commands a dominant 61% market share in India's coal and mineral consultancy sector (FY2025), with no close second competitor. It holds the status of a Mini Ratna Category-I PSU and serves as the strategic technical arm for both Coal India Limited and the Ministry of Coal.

Central Mine Planning & Design Institute Limited (CMPDI) is India's foremost mining consultancy and engineering services company, set up in 1974 as a wholly-owned subsidiary of Coal India Limited (CIL) — the world's largest coal producer. Headquartered in Ranchi, Jharkhand, CMPDI provides end-to-end technical consultancy across the entire value chain of coal and mineral resource development.

IPO Snapshot

Company Name

Central Mine Planning & Design Institute Limited (CMPDI)

Sector

Mining Consultancy & Engineering Services

Industry

PSU / Government — Coal & Minerals

Established

1974 (incorporated as Coal India subsidiary in 1975)

Headquarters

Gondwana Place, Kanke Road, Ranchi, Jharkhand

Promoter

Coal India Limited (Govt. of India Enterprise)

Issue Size

₹1,842.12 Crore

Fresh Issue

Nil (100% Offer for Sale)

Offer for Sale

10,71,00,000 equity shares

Market Cap After Listing

~₹12,280 Crore

Promoter Holding (Pre-IPO)

100%

Promoter Holding (Post-IPO)

~85%

Retail Quota (RII)

35% — 3,74,85,000 shares

QIB Quota

50% — 5,35,50,000 shares

NII / HNI Quota

15% — 1,60,65,000 shares

Employee Reservation

53,55,000 shares

Shareholder Quota (Coal India)

1,07,10,000 shares

Book Running Lead Managers

IDBI Capital Markets & Securities Ltd; SBI Capital Markets Ltd

Registrar

KFin Technologies Ltd

Anchor Investors Round

₹469.74 Cr from 22 anchors (Mar 18, 2026)

Key Anchor Investors

LIC, Nippon India MF, ICICI Prudential MF, Edelweiss MF, Goldman Sachs, Citigroup, BNP Paribas, GIC, Societe Generale

Status

Mini Ratna Category-I PSU

REVENUE SEGMENTS

Business Vertical

Revenue Share (FY25)

Geological Exploration & Resource Evaluation

46.2%

Mine Planning & Design Services

~25%

Environmental Planning & Monitoring Services

~15%

Geomatics, Remote Sensing & Survey Services

~14%

KEY CLIENTS & CUSTOMER CONCENTRATION

CMPDI's revenue is heavily concentrated among government entities. Coal India Limited and its subsidiaries contributed 67.1% of revenue in FY2025 (down from 80.2% in FY2024, showing early signs of diversification). Government entities/agencies as a whole account for ~97.8% of total revenues. The top 10 clients cumulatively contribute approximately 95% of revenues.

INFRASTRUCTURE & SCALE

One of India's largest fleets of exploratory drilling equipment for coal & mineral exploration (as of March 31, 2025).

Seven Regional Institutes across coal-producing states — Madhya Pradesh, Chhattisgarh, Odisha, and West Bengal.

Eight advanced testing laboratories spread across coalfields in India.

Capability to plan open-cast mines with annual production up to 85 million tonnes; mining depths up to 420 metres.

Active participation in NMET-funded drilling and exploration for non-coal minerals (bauxite, copper, zinc, magnetite, and more).

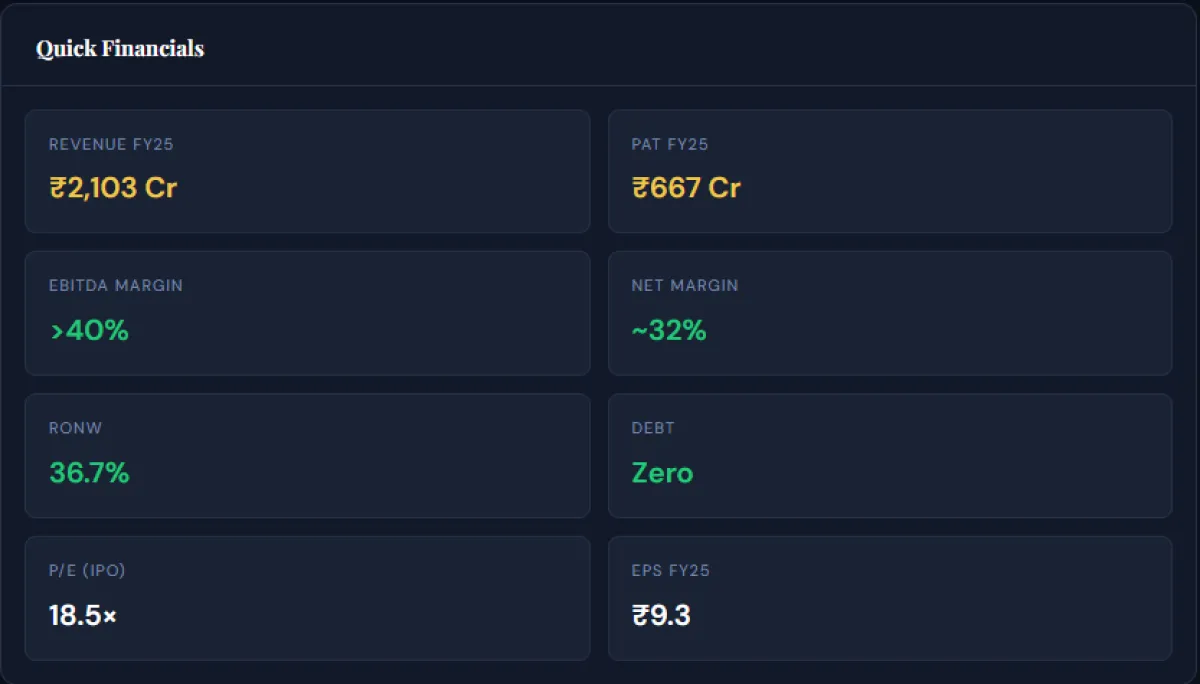

FINANCIAL PERFORMANCE

Metric

FY2023

FY2024

FY2025

9M FY26*

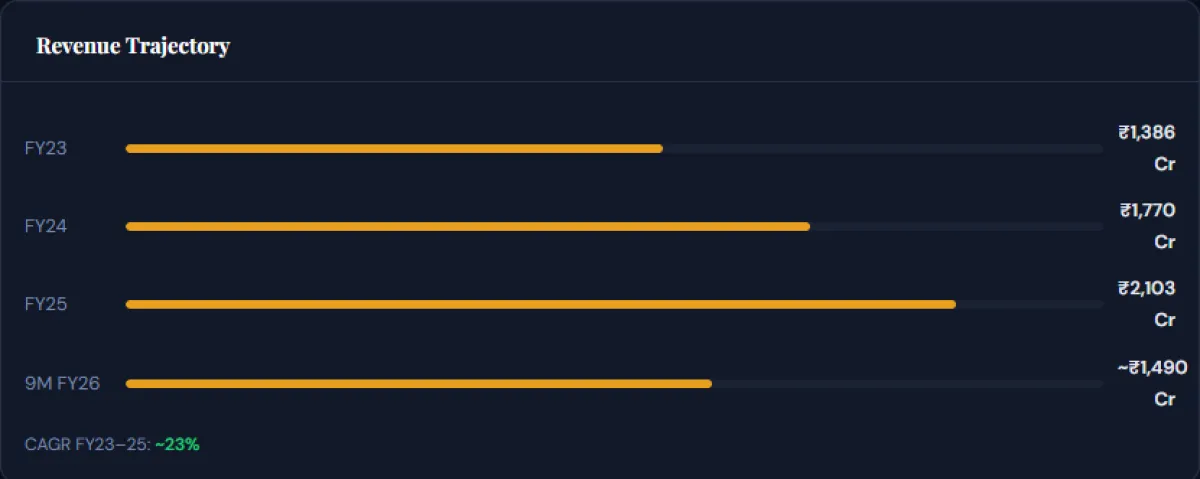

Revenue from Operations (₹ Cr)

1,386.1

1,770.2

2,102.8

~1,490

Total Revenue incl. Other Income (₹ Cr)

—

1,770.2

2,177.5

—

EBITDA (₹ Cr)

~580

~760

~900+

—

EBITDA Margin

~42%

~43%

>42%

—

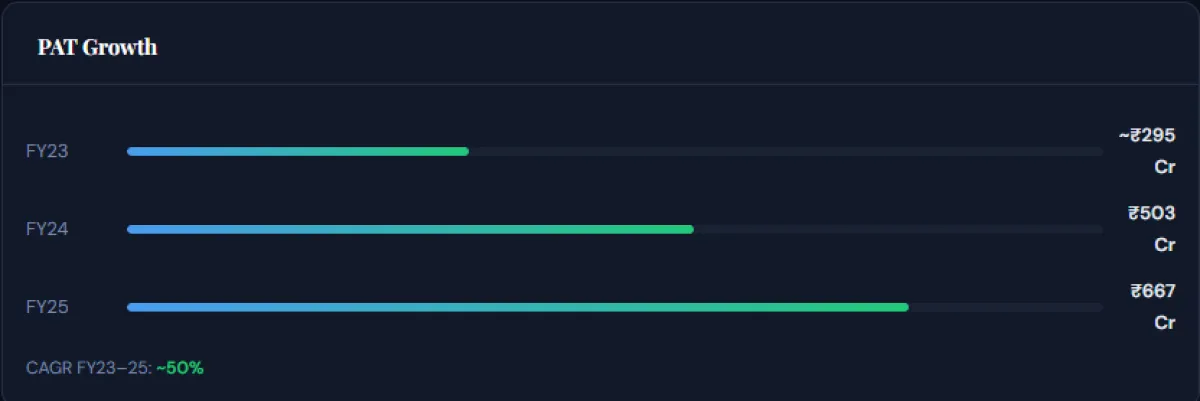

Net Profit / PAT (₹ Cr)

~295

503.2

666.9

—

EPS (₹)

~4.2

~7.1

9.3

—

Total Debt (₹ Cr)

Nil

Nil

Nil

Nil

Net Worth (₹ Cr)

—

~1,400

~1,820

—

* 9M FY26 refers to the nine months ended December 31, 2025. Exact EBITDA figures are estimated based on reported operating margins. Source: Company RHP, IPOWatch, JM Financial.

FINANCIAL TREND ANALYSIS

Revenue CAGR of ~23%from ₹1,386 crore (FY23) to ₹2,103 crore (FY25) reflects strong demand for mining consultancy driven by India's energy security push.

PAT grew ~50% CAGR(FY23–25), from ~₹295 crore to ₹667 crore — significantly outpacing revenue growth, reflecting strong operational leverage.

Margins above 40% consistently— rare for a PSU and comparable to top-tier IT services companies.

Completelydebt-freebalance sheet as of December 31, 2025 — zero borrowings.

Dividend-paying PSU following Ministry of Finance dividend guidelines.

KEY FINANCIAL RATIOS

Ratio / Metric

Value

Signal

P/E Ratio (IPO — Upper Band)

~18.5×

Strong (Discount to Peers)

Industry Peer Avg P/E

22.6×

Reference

Price / Book (P/B) Ratio

~6.7×

Neutral

ROE / RoNW (FY25)

36.7%

Strong

Weighted Avg. RoNW

34.8%

Strong

ROCE

>35%

Strong

Debt / Equity Ratio

0.00

Excellent (Debt-Free)

EBITDA Margin

>40%

Strong

Net Profit Margin

~30–32%

Strong

Revenue Growth (YoY FY24→25)

+23%

Strong

PAT Growth (YoY FY24→25)

+33%

Strong

EPS (FY25)

₹9.3

Healthy

Market Cap / Revenue

~5.8×

Neutral

Fresh Issue Dilution

Zero

No Dilution

VALUATION ANALYSIS & PEER COMPARISON

At the upper price band of ₹172 per share, CMPDI is valued at approximately ₹12,280 crore in market capitalization. Based on FY2025 EPS of ₹9.3, the implied P/E multiple is approximately 18.5× — a meaningful discount to both comparable listed PSU peers and the industry peer average of 22.6× cited in the RHP.

More notably, CMPDI's RoNW of 36.7% substantially exceeds both identified peers, suggesting the stock may be attractively priced relative to its capital efficiency and profitability metrics.

Company

Market Cap

P/E

RoNW

Revenue (FY25)

CMPDI (IPO Price)

~₹12,280 Cr

~18.5×

36.7%

₹2,103 Cr

Engineers India Ltd (EIL)

~₹10,500 Cr

~22×

23.5%

~₹3,800 Cr

RITES Limited

~₹9,200 Cr

~23×

15.5%

~₹2,700 Cr

Industry Peer Avg (RHP)

—

22.6×

—

—

Note: Peer data sourced from company RHP (Basis for Offer Price section) using BSE closing prices as of March 5, 2026. CMPDI P/E based on FY25 EPS at upper band. All figures are approximate.

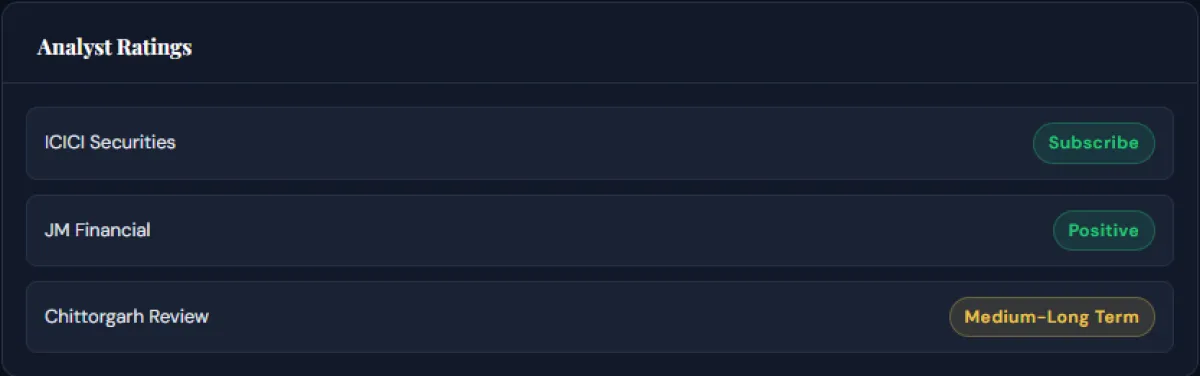

ICICI Securities has assigned a Subscribe rating, noting the IPO appears attractive at ~18× P/E given strong double-digit margins, healthy return ratios, debt-free balance sheet, and robust growth prospects.

It is worth noting that the issue is entirely an OFS — the company receives zero fresh capital. All ₹1,842 crore proceeds go to the selling shareholder (Coal India Limited).

KEY STRENGTHS

Dominant 61% Market Sharein India's coal and mineral consultancy sector — deeply entrenched with no close competitor. This moat has been built over five decades of institutional knowledge.

Strategic PSU Backing— Coal India and Ministry of Coal provide institutional stability, guaranteed order flow, government policy priority, and de-facto preferred vendor status.

Exceptional Financials— Revenue CAGR of 23%, PAT CAGR of ~50%, EBITDA margins consistently above 40%, and a completely debt-free balance sheet (as of Dec 31, 2025).

Valuation Discount to Peers— P/E of ~18.5× at IPO price vs industry average of 22.6×, while CMPDI's RoNW of 36.7% exceeds both comparable peers (EIL: 23.5%, RITES: 15.5%).

Multidisciplinary Expertise— Comprehensive service offerings spanning geological exploration, mine planning, environmental management, geomatics, infrastructure engineering, and management systems under one roof.

Advanced Infrastructure— One of India's largest exploratory drilling fleets; eight laboratories; seven regional institutes across key coal-producing states.

Non-Coal Diversification Underway— Active diversification into UCG (Underground Coal Gasification), CBM (Coal Bed Methane), non-coal minerals (bauxite, copper, zinc, magnetite), and international consultancy.

Government Energy Policy Tailwind— India's push for energy security, scientific mining, and mineral exploration aligns directly with CMPDI's service offerings.

Consistent Dividend Payer— Follows Ministry of Finance guidelines for dividend payout, rewarding shareholders consistently.

KEY RISKS

Extreme Customer Concentration— Coal India and its subsidiaries contributed 67.1% of FY25 revenues. Top 10 clients account for ~95% of revenues. Loss of any key client could materially impact financials.

Near-Total Government Revenue Dependence— 97.8% of revenues derive from government entities/agencies. This exposes the company to regulatory risk, delayed receivables, and policy change sensitivity.

Coal Sector Concentration— Geological exploration services alone contributed 46.2% of FY25 revenues. A structural decline in coal demand due to India's energy transition could impact long-term growth.

Pure OFS — Zero Capital Inflow— All IPO proceeds go to Coal India (selling shareholder). No funds raised for business expansion, debt repayment, or operational improvement by the company itself.

Government Policy & Funding Risk— Drilling and exploration activities significantly depend on funding from the Ministry of Coal and NMET (National Mineral Exploration Trust). Policy changes or funding delays could impact operations.

Vendor Concentration in Exploration— Exploration activities depend on a limited number of vendors for services such as core drilling, geophysical logging, and borehole testing.

Energy Transition Risk— India's long-term commitment to renewable energy and net-zero targets may gradually reduce the strategic importance of coal consultancy over a 10–15 year horizon.

PSU Operational Constraints— As a government entity, CMPDI may face limitations in talent acquisition, salary flexibility, and operational agility compared to private sector peers.

IPO SUBSCRIPTION DATA (Day 1)

Subscription data as of end of Day 1 (March 20, 2026, 5:05 PM IST). Note: QIBs and large HNIs typically apply on the final day.

Category

Shares Offered

Shares Bid

Subscription

Retail Individual Investors (RII)

3,74,85,000

~3,74,85,000 × 0.10

0.10×

Non-Institutional Investors (NII)

1,60,65,000

~1,60,65,000 × 0.05

0.05×

— S-HNI (Small)

—

—

0.08×

— B-HNI (Large)

—

—

0.03×

Qualified Institutional Buyers (QIB)

5,35,50,000

—

0.00×

Overall

7,97,89,500

~48,06,240

0.07×

⚠ Day 1 subscription of PSU IPOs is typically low. QIBs and large HNIs conventionally wait until the final session on Day 3. The anchor round (₹470 Cr from 22 institutions including LIC, Goldman Sachs, Citigroup) signals strong institutional interest. Final subscription data will be available post March 24, 2026.

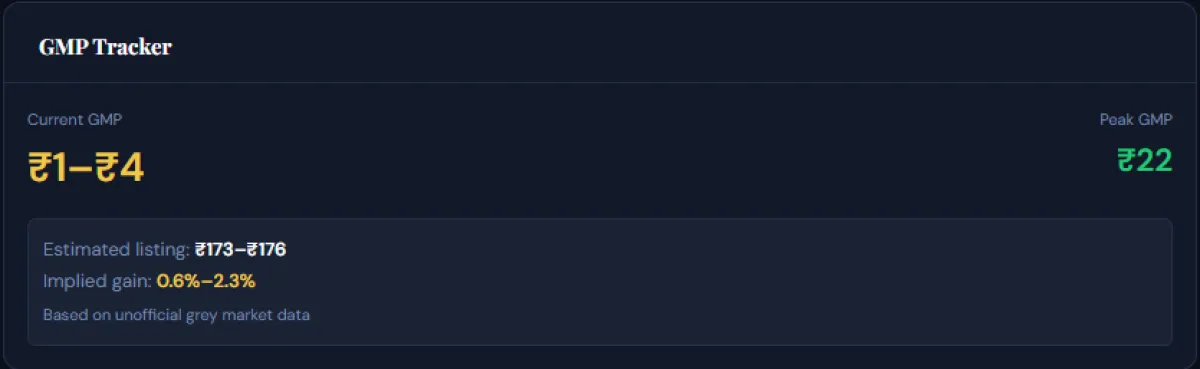

GRAY MARKET PREMIUM (GMP)

GMP data is unofficial and indicative only. It reflects informal market sentiment, not guaranteed listing price.

Metric

Value

IPO Issue Price (Upper Band)

₹172

GMP — Peak (before opening)

₹22–₹24

GMP — Current (as of Mar 20, 2026)

₹1–₹4

Estimated Listing Price (GMP basis)

₹173–₹176

Estimated Listing Gain %

0.58% – 2.3%

Unlisted Market Trade Price

~₹173.5–₹176

GMP touched a high of ₹22 on March 17 but has cooled significantly by opening day, reflecting modest short-term listing gain expectations. The cooling GMP trend suggests the market is pricing this more as a long-term hold than a quick listing-gain trade. This is characteristic of large-cap PSU IPOs.

OBJECTS OF THE ISSUE

Since this IPO is a 100% Offer for Sale (OFS), the company (CMPDI) will not receive any proceeds from the issue. The entire net proceeds will be received by the Promoter Selling Shareholder — Coal India Limited.

Purpose

Amount

% of Issue

Proceeds to Coal India Limited (Selling Shareholder)

₹1,842.12 Cr

100%

Proceeds to CMPDI (Company)

Nil

0%

The RHP states: "Our company expects that listing of the equity shares will enhance our visibility and brand image and provide liquidity and a public market for the equity shares in India." The listing creates a public market for shares but injects no capital into the operating company.

FINAL SUMMARY

Business Quality: CMPDI is a structurally strong business with a virtually unassailable competitive position — 61% market share, five decades of institutional knowledge, government backing, and a diversified yet specialized service portfolio. The company's role as the technical backbone of India's coal and mineral sector gives it a quasi-monopoly status in its niche.

Financial Strength: The financial profile is exceptional for a PSU. Revenue CAGR of 23%, PAT CAGR of ~50%, EBITDA margins consistently above 40%, zero debt, and strong return ratios (RoNW ~36.7%) — all indicators of a high-quality, capital-efficient business. The company generates strong free cash flows and pays regular dividends.

Valuation: At a P/E of ~18.5× (FY25 basis), the IPO appears attractively priced relative to comparable PSU consultancy peers (EIL at ~22×, RITES at ~23×) and the RHP-cited industry average of 22.6×. The superior return profile (RoNW significantly above peers) suggests a potential undervaluation relative to intrinsic quality.

Key Considerations: The 100% OFS nature means zero capital enters the business. Customer concentration (top 10 clients = ~95% revenues; CIL = ~67%) is a notable structural risk. Long-term energy transition risk is real, though medium-term coal dependency and India's mineral exploration push provide a clear runway for 5–10 years.

⚠ Disclaimer: This report is for informational and educational purposes only. It does not constitute investment advice. Investors should review the Red Herring Prospectus (RHP) available on the SEBI website and consult a SEBI-registered financial advisor before making any investment decision.

LISTING PROBABILITY ANALYSIS

Based on available GMP trends, Day 1 subscription levels, anchor investor quality, and sector/market sentiment, here is a probability assessment for various listing outcomes:

Listing at Premium (>5% gain)Low – Medium

Listing near IPO Price (±2%)Medium – High

Listing at Discount (below issue price) - Low

Factor

Indicator

Signal

Current GMP

₹1–₹4

Neutral

GMP Peak

₹22–₹24

Cooled significantly

Day 1 Subscription

0.07×

Typical for PSU

Anchor Investor Quality

LIC, Goldman Sachs, Citigroup

Strong

Sector Momentum

Mining / PSU

Moderate

Valuation vs Peers

Discount (~18.5× vs 22.6×)

Favourable

ICICI Securities Rating

Subscribe

Positive

Listing Type

Long-term PSU Hold

Medium-Term Value

The tepid GMP and slow Day 1 subscription are not unusual for large-cap PSU IPOs. Given high-quality anchors, attractive valuation versus peers, and strong fundamentals, the listing is more likely to be stable to marginally positive rather than a sharp premium or discount.

**Disclaimer: We are not SEBI registered. The content provided is for educational and informational purposes only and should not be considered investment advice. Stock market investments are subject to market risks. Please consult a SEBI-registered financial advisor before making investment decisions.**

InvesTalks is a powerful market learning and analysis platform built for traders, investors, and finance enthusiasts. Stay updated with real-time market insights, expert blogs, educational content, and smart investing strategies — all in one place.

ITS InvesTalks uses cookies to enhance your experience,

analyze traffic, and display relevant advertisements.

You can accept all cookies or manage your preferences.

Login to comment.